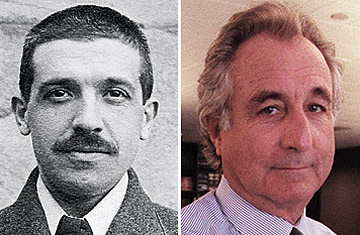

(l. to r.) Charles Ponzi and Bernard Madoff.

The $50 billion Ponzi scheme allegedly masterminded by former Nasdaq chairman Bernard Madoff punctuated a miserable year for Wall Street in the worst possible way: by underlining, yet again, that savvy market-makers can harness arcane financial instruments as weapons of mass destruction. Left in Madoff's wake are bankrupt investors, mortified regulators and a raft of unnoticed red flags. Madoff's methods previously had been investigated by the SEC, and in 2001, a prescient article raised questions about his inscrutable strategies: "Madoff's investors rave about his performance — even though they don't understand how he does it," wrote Barron's Erin Arvedlund, who quoted a "very satisfied investor" as conceding, "Even knowledgeable people can't really tell you what he's doing." But for investors pocketing windfalls, the lure of easy money outstripped suspicions raised by Madoff's shroud of secrecy. When that shroud was lifted, however, Madoff's investment fund stood revealed as a classic Ponzi scheme: a con game in which the illusion of solvency was created by paying off early investors with capital raised from later entrants. As long as new investment continued to come in the door, the earlier adopters reaped fat rewards; once markets tumbled and investors withdrew, however, the whole thing collapsed like a house of cards.

Though a Boston businessman named Charles Ponzi was the scam's namesake, he wasn't its original practitioner. According to Mitchell Zuckoff, a Ponzi biographer, the reigning king of the "rob Peter to pay Paul" scam was a New York grifter named William Miller, who bilked investors out of $1 million — nearly $25 million in today's dollars — in 1899. After drumming up interest by claiming to have an inside window into the way profitable companies operated, Miller — who earned the nickname "520 percent" due to the astonishing rate of return he promised investors over the course of a year — salted his scam by paying out the first few investors. After his racket was exposed by a newspaper investigation, he was sentenced to 10 years in prison. According to Zuckoff, his creditors got just 28 cents back for every dollar they'd invested. (See the top 10 scandals of 2008.)

Ponzi was a charismatic Italian immigrant who, in 1919 and 1920, coaxed thousands of people into shelling out millions of dollars — including a staggering $1 million in a single three-hour period — to buy postage stamps using international reply coupons. This strategy, Ponzi promised, enabled one to purchase postage at European currencies' lower fixed rates before redeeming them in U.S dollars at higher values. "For instance," Zuckoff explained in a Dec. 15 article for FORTUNE, "a person could buy 66 International Reply Coupons in Rome for the equivalent of $1. Those same 66 coupons would cost $3.30 in Boston," where Ponzi was based. But there weren't enough coupons in circulation to make the plan workable. The ploy bore the hallmarks of both Miller's scheme and others to follow it: it trumpeted the possibility of massive gains (Ponzi promised a 50% return in just 90 days), parried questions about its legitimacy by paying out the first few investors, and collapsed when Ponzi couldn't rustle up enough fresh marks to keep up with the money going out the door.

Ponzi, who was released from prison and deported back to Italy in 1934, set the standard in the genre. But the golden age of Ponzi and pyramid schemes didn't arrive for decades. (The two highly similar cons are often conflated, though in Ponzi schemes, a ringleader facilitates the entire enterprise; in a pyramid scheme, rungs of collaborators recruit new investors.) In the boom years of the 1980s and '90s, as traders developed increasingly sophisticated investment vehicles, the cons cropped up with increasing regularity. In 1985, a San Diego currency trader named David Dominelli was revealed to have fleeced more than 1,000 investors to the tune of $80 million. During the 1990s, a Florida church called Greater Ministries International bilked nearly 20,000 people out of $500 million in a pyramid scheme hatched by leader Gerald Payne, who claimed God would double the money of pious investors. (Dominelli pleaded guilty and was sentenced to 20 years in prison, while Payne was convicted and sentenced to 27.) The spate of incidents wasn't limited to the U.S., either. When communism crumbled in Eastern Europe, one of the earliest side effects of free-market capitalism was the proliferation of people looking to get rich quick. In Albania, under Communism the poorest nation in Europe, citizens sank some $1.2 billion dollars into pyramid schemes in 1996. When they collapsed the following year, investor outrage brought down the government.

This ignominious group has had some high-profile recent entrants, including Democratic fundraiser Norman Hsu, who was charged in October with operating a $60 million Ponzi fraud, and former boy-band impresario Lou Pearlman, who in addition to foisting N'Sync on an unsuspecting public also stole $300 million in investor capital over two decades. Earlier this month, Minnesota businessman Tom Petters was indicted by a federal grand jury on 20 counts of fraud, conspiracy and money laundering stemming from his alleged role in a 13-year, $3.5 billion Ponzi ring. Still, the $50 billion fraud Madoff allegedly perpetrated is the most egregious Ponzi scheme to date—unless you subscribe to an argument advanced by financial consultant Janet Tavakoli. In a neat summary of the anger millions of people are channeling toward Wall Street, Tavakoli wrote on her company website: "The largest Ponzi scheme in the history of the capital markets is the relationship between failed mortgage lenders and investment banks that securitized the risky overpriced loans and sold these packages to other investors—a Ponzi scheme by every definition applied to Madoff." By comparison, she wrote, the fallen fund manager is just "a piker."