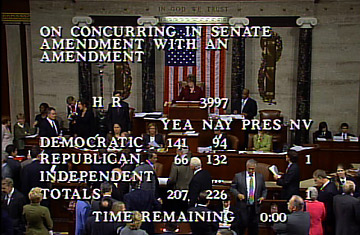

This video image provided by the House of Representatives shows the vote on the emergency financial-rescue package

By voting down the proposed $700 billion financial bailout package — and causing a spectacular stock market rout — a majority of members in the House of Representatives made a clear statement that they didn't want to put taxpayers on the hook for the failures of financial institutions.

But there's a catch: taxpayers are already on the hook for the failures of financial institutions, and it's possible that the bill will actually be larger without bailout legislation than with it. That's because the regulators who mind the financial industry — the Federal Reserve, Treasury and FDIC — will keep doing what they've been doing: stepping in to prevent the chaotic failure of banks and other large financial institutions. This means continuing to put hundreds of billions of taxpayer dollars at risk, but in a way that adheres to no clear plan of action and doesn't require members of Congress to explicitly approve their actions.

On Monday afternoon, Wall Street basically stopped trading to watch TV — mainly CNBC — to see how the House of Representatives would vote on the $700 billion bailout package. When it first started looking like the bill would fail, the Dow plummeted 389 points, or 3.6%, in just seven minutes. If it had continued at that pace for much longer, this would have been perhaps the most harrowing day in stock market history. It didn't, but things were still really, really bad. The Dow ended the day down 778 points, or 7%, and the S&P 500 — a better measure of the overall market — was down 107 points, or 8.8%, its worst performance since the 1987 market crash. And markets for bonds and short-term loans were, for the most part, nonexistent.

So what happens now? On Capitol Hill, House leaders said they'll try again soon. Treasury Secretary Henry Paulson practically begged for a revised deal in his brief appearance after the market carnage. "Our tool kit is substantial but insufficient," he said. The market's traumatized reaction today may change some minds and some votes.

In asking Congress 11 days ago for the authority to spend up to $700 billion to buy troubled assets, Paulson and Fed Chairman Ben Bernanke were hoping to share some of the responsibility and the blame — and get the freedom to boost companies that weren't already on the brink of failure. Instead, they're back to being crisis managers for the moment — and maybe for the duration of the crisis.

That's not all bad, especially now that most of the endangered financial institutions are commercial banks. The Federal Government has clearly defined that authorities take them over, merge them out of existence or shut them down — whereas it had to make things up as it went along with investment banks Bear Stearns and Lehman Brothers and insurer AIG. That's why the demise of giant banks Washington Mutual and Wachovia, arranged over the past week by the FDIC, occurred in a far more orderly fashion than the non-bank meltdowns.

But orderly isn't the same as cheap. To get Citigroup to absorb Wachovia, the FDIC agreed to share the risk on a $312 billion portfolio of loans (Citi has to eat the first $42 billion in potential losses; anything above that hits the FDIC fund).

Also, the fact that every big FDIC deal so far in this crisis has been different — IndyMac was allowed to fail, with only insured deposits safe; WaMu was seized, but all depositors were protected; and Wachovia was sold in a deal that protected both depositors and owners of the company's bonds but left shareholders with very little — has left investors guessing about the fate of the rest of the banking world. Hardest hit in today's market sell-off were regional banks like Sovereign Bancorp and National City, perhaps because they seem too small to get special FDIC treatment.

Federal authorities are going to keep doing whatever they can to keep the financial system from collapsing. Taxpayers will bear the risks and the costs of that, whether Congress votes to put them there or not. And it's possible — although nobody can know for sure — that this ad hoc approach will end up costing more than an up-front $700 billion bailout.

(See the ten steps to the financial meltdown here and TIME's photos of the global financial crisis here.)