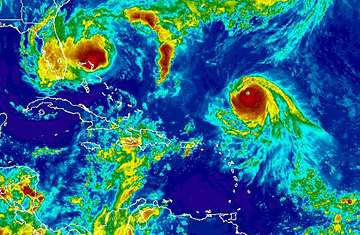

Tropical Storm Hanna passes the edge of the Bahamas as Hurricane Ike, a still-more-dangerous Category 4 storm, advances from the east.

As Hurricane Ike barrels toward South Florida, Americans can be sure they won't have to endure another catastrophic failure of a hurricane protection system. That's because South Florida doesn't have a hurricane protection system. As South Floridians like to say: Ay dios mio! Ike is now scheduled to pass just south of Miami as a Category 4 storm; National Hurricane Center researchers recently concluded that a Cat 4 hitting Miami could cause $70 billion in damage. To use another South Florida-ism: Oy vey!

Dangling into the Gulf like a continental afterthought, Florida has always been Mother Nature's favorite American target, absorbing eight named storms in 2004 and 2005 alone. The state has gotten better at preparing for hurricanes, with stricter building codes and well-rehearsed evacuation plans. But it's still dangerously exposed — not only to the elements, but to financial ruin. It's got the nation's most dysfunctional property insurance market, a byproduct of life in harm's way. Fitch's ratings agency concluded in March that if a big storm hits Florida, "the fragile market could effectively collapse."

Ike could well be a Gustav-like bust rather than a Katrina-like disaster (See photos of Hurricane Gustav here). But eventually, disaster will visit the peninsula, and it's still not clear who's going to pay the tab. "It's going to be a financial nightmare," says Cecil Pearce of the American Insurance Association. "Florida is the nation's basket case."

It's not that Florida's vulnerability is a secret. Florida homeowners pay some of the nation's highest insurance premiums; in a recent poll, despite a housing crisis, an economic crisis, a water crisis and an environmental crisis, Floridians named those premiums their number-two concern about the state's future, behind property taxes but ahead of jobs, education, health care and the dying Everglades.

Since Hurricane Andrew put most Florida insurers out of business and scared several national insurers out of the state, the state government has helped to hedge the risk of hurricanes. It provides subsidized insurance to 1.3 million high-risk homeowners who can't get private policies, an increase of more than 50% in just three years. It also has a Hurricane Catastrophe Fund that provides subsidized reinsurance to the state's private firms.

But a series of studies have made it clear that if the Big One or even a Pretty Big One strikes, Florida is going to have very serious problems. The state-run insurance firm and the Catastrophe Fund have just a few billion dollars on hand, so a major storm would force both entities to float massive bond issues in an unfavorable market, and to make up their shortfalls through gigantic assessments on policyholders. A House committee recently warned that the state would have "extreme difficulty paying its obligations" after a 100-year storm, and that premiums on nearly every property, car and business could skyrocket. A report for the state Office of Insurance Regulation found that even a 50-year storm would cause extreme financial stress, especially given the current credit crunch.

Industry actuaries say the problem is simple: Florida's insurance rates, high as they may be, are not high enough for a state with an estimated 25% of America's high-risk property. Reinsurance rates are soaring, and private insurers like State Farm and Allstate have scaled back in Florida, forcing an additional 500,000 customers into the state pool. "For some areas in Florida, insurance companies could not obtain reinsurance at any price," Insurance Commissioner Kevin McCarty recently told Congress. And last year, Republican Governor Charlie Crist pushed through reforms to decrease premiums, a politically popular move that will create even more pressure if disaster strikes. "I get the concerns," Crist recently told me. "But we're not going to stand for gouging."

The gouging fears are understandable; McCarty told Congress that some insurers have insisted on 25% profit margins, while using computer models that overstate risk. But no one denies that the risk is real: it's been 80 years since a major storm hit a major Florida city, but hurricane researchers have calculated that the next one could cause as much as $150 billion worth of damage. And Crist's reforms, while reducing premiums, included other changes that increased the risk that taxpayers and policyholders will have to bail out the Cat Fund. "The risk was removed from the insurers' portfolio and is now being supported by the people of Florida," McCarty explained.

That's why Crist and just about every other Florida politician is pushing for a national catastrophe insurance fund, which would shift some of that risk to federal taxpayers. But the idea is not so popular with other states, for the obvious reason that other states don't have as much risk. Florida has spent the last 80 years ignoring its vulnerability, developing its floodplains and shorelines, selling the dream of the Sunshine State to northerners and foreigners. But the day of reckoning will come.

Hopefully it won't come Tuesday.